UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the fiscal year ended

For the transition period from _______ to ______

Commission

File Number:

| (Exact name of registrant as specified in its charter) |

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

(Address of principal executive office)

Registrant’s

telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant

to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit and post such files).

Indicate by check mark whether the registrant is a large, accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |

| ☒ | Smaller reporting company | |||

| Emerging growth company |

If

an emerging growth company, indicated by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐

The

aggregate market value of the shares of voting and non-voting common stock held by non-affiliates of the Registrant as of June 30,

2022 , the last business day of the Registrant’s last completed second quarter, based upon the closing price of $0.0044 per

share as reported by the OTC Pink on such date was $

As of April 4, 2023, shares of common stock are issued, and outstanding.

Documents

incorporated by reference:

TABLE OF CONTENTS

Forward-Looking Statements

This Report contains predictions, estimates and other forward-looking statements that relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue” or the negative of these terms or other comparable terminology.

Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. Forward-looking statements represent our management’s beliefs and assumptions only as of the date of this Annual Report. You should read this Report and the documents that we have filed as exhibits to this Report completely and with the understanding that our actual future results may be materially different from what we expect.

All forward-looking statements speak only as of the date on which they are made. We undertake no obligation to update such statements to reflect events that occur or circumstances that exist after the date on which they are made, except as required by federal securities and any other applicable law.

| 2 |

PART I

Item 1. Business

Overview

InnovaQor, Inc., a Nevada corporation (“InnovaQor” or the “Company”), provides information technology solutions and services to healthcare and laboratory customers in the United States. Our goal is to develop and deliver a technology-based medical professional’s network communication platform to a broad range of healthcare professionals and businesses using a subscription revenue model with added value bolt on services. The Company, through an acquisition that closed on June 25, 2021, has a number of fully developed products and services which it offers through six wholly owned subsidiaries that provide medical support services primarily to clinical laboratories, corporate operations, rural hospitals, physician practices and behavioral health/substance abuse centers.

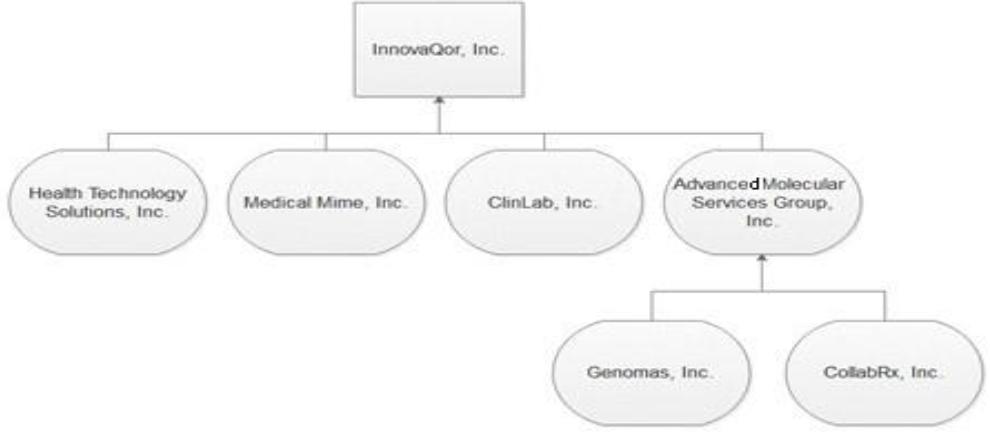

The Company has the following wholly owned subsidiaries, which it purchased on June 25, 2021: Health Technology Solutions, Inc., Medical Mime, Inc., ClinLab, Inc., Advanced Molecular Services Group, Inc. (“AMSG”), Genomas, Inc. and CollabRx, Inc. These subsidiaries provided products and services to 25 and 36 customers in the United States and generated $343,440 and $468,883 (including $191,517 and $237,551 from a related party) in net revenues during the years ended December 31, 2022 and 2021, respectively.

Health Technology Solutions, Inc. (“HTS”): HTS provides virtual chief information officer (vCIO), IT managed services and data analytics dashboards to our subsidiaries and outside medical service providers. HTS operates from the corporate offices in West Palm Beach, Florida.

Medical Mime, Inc. (“Mime”): Mime was formed on May 9, 2014. It specializes in electronic health records (EHR) software and subscription services for the behavioral health and rehabilitation market segments. It currently serves ten behavioral health/substance abuse facilities.

ClinLab, Inc. (“ClinLab”): ClinLab develops and markets laboratory information management systems to mid-size clinical laboratories. It currently services eight clinical laboratories across the country.

AMSG owns CollabRx, Inc. (“CollabRx”) and Genomas, Inc. (“Genomas”), each of which is an inactive operation.

Genomas operated a diagnostics lab until December 31, 2019, and was focused solely on the pharmacogenomics technology and platform, MedTuning, to interpret diagnostics outcomes and translate these outcomes into easily usable information to indicate the effectiveness of medications for a patient. This solution would require minimum effort to be back in operation. CollabRx owns a technology platform and database for interpreting diagnostics outcomes from cancer patients that could match the result to known treatments and or clinical trials. This solution has been dormant for a number of years and to be viable in the marketplace will require updates to the technology and the database.

Each of the subsidiaries is wholly owned by the Company and complements each other, allowing for cross selling of products and services. The Company believes the current solutions will become an added value option to a technology-based medical professional’s network communication platform to a broad range of healthcare professionals and businesses using a subscription revenue model with added value bolt on services the Company plans to develop.

In the coming year we plan to develop, acquire, or license and offer a telehealth solution through corporate partnerships in the emerging health technology sector.

Cautionary Statement Concerning Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements. Statements contained herein that refer to the Company’s estimated or anticipated future results are forward-looking statements that reflect current perspectives of existing trends and information as of the date of this filing. Forward-looking statements generally will be accompanied by words such as “anticipate,” “believe,” “plan,” “could,” “should,” “estimate,” “expect,” “forecast,” “outlook,” “guidance,” “intend” “may,” “might,” “will,” “possible,” “potential,” “predict,” “project,” or other similar words, phrases or expressions. Such forward-looking statements include statements about the Company’s plans, objectives, expectations and intentions. It is important to note that the Company’s goals and expectations are not predictions of actual performance. Actual results may differ materially from the Company’s current expectations depending upon a number of factors affecting the Company’s business. These risks and uncertainties include those set forth under “Risk Factors” beginning on page 11, as well as, among others, business effects, including the effects of industry, economic or political conditions outside of the Company’s control; the inherent uncertainty associated with financial projections; the anticipated size of the markets and demand for the Company’s products and services; the impact of competitive products and pricing; and access to available financing on a timely basis and on reasonable terms. We caution you that the foregoing list of important factors that may affect future results is not exhaustive.

| 3 |

When relying on forward-looking statements to make decisions with respect to the Company, investors and others should carefully consider the foregoing factors and other uncertainties and potential events and read the Company’s filings with the Securities and Exchange Commission (the “SEC”) for a discussion of these and other risks and uncertainties. The Company undertakes no obligation to update or revise any forward-looking statement, except as may be required by law. The Company qualifies all forward-looking statements by these cautionary statements.

Company History

The Company was originally incorporated in the State of Nevada on September 7, 1999, under the name Ancona Mining Corporation. The Company’s name was changed to VisualMED Clinical Solutions Corporation on November 30, 2004, from Ancona Mining Corporation.

The Company’s name was changed to InnovaQor, Inc. on September 8, 2021, from VisualMED Clinical Solutions Corporation. VisualMED was a medical information company that used technology to assist physicians and nurses streamline the mass of patient information in a coherent and usable manner. Its clinical information systems were designed for use in hospitals, healthcare delivery organizations and regional and national healthcare authorities. In response to changes in the marketplace, the Company then sought to take its applications originally created for clinicians and make them available to patients and individuals concerned about their health. As part of this process the Company partnered with various consultants to consider the medical applications, develop a marketing strategy and investigate how best to transition its existing applications to upgraded versions, including integrating artificial intelligence for data assessment and outcomes. With the onset of the COVID-19 pandemic, however, it became apparent that this business opportunity would require more capital, management capability and time than what was available to the Company.

In late 2020, the majority of shareholders and the Board of Directors charged management of VisualMED to find a new business opportunity for the Company that would allow it to leverage its healthcare, software and IT experience. At the beginning of 2021, the Company initiated measures that would facilitate a new opportunity for the Company. Subsequently, in May 2021, then CEO Gerard Dab entered into an agreement with and engaged the services of Epizon Limited (“Epizon”), a Nassau, Bahamas, based management consulting company specializing in the provision of management services to secure financing and opportunities for growth. Seamus Lagan, the Chief Executive Officer of Rennova Health, Inc. (“Rennova”), the company we ultimately completed a transaction with, is also the managing director of Epizon.

The objective of the agreement with Epizon was to help VisualMED find a new opportunity in its core healthcare technology business. The Company needed to find and develop new products that would be more relevant for a changing healthcare marketplace. Epizon was engaged to assist VisualMED with its capital structure, and to look for new business opportunities and/or acquisitions that could result in improved shareholder value. The terms of the agreement with Epizon called for the transfer to Epizon of 1,000 shares of Series A-1 Supermajority Voting Preferred Stock (the “Series A-1 Preferred Stock”), with a stated value of $10.00 each, personally owned by Gerard Dab, on the successful completion of a transaction as defined in the agreement. It was determined that an agreement with Rennova was the most viable opportunity available to VisualMED. The conditions of the Epizon agreement were met and the transfer of shares of Series A-1 Preferred Stock was completed. This transfer resulted in a change of voting control of VisualMED, as the Series A-1 Preferred Stock, in the aggregate, has the right to the number of votes equal to 51% of the votes entitled to be cast at a meeting or to vote by written consent. As the owner of the Series A-1 Preferred Stock, Epizon will be able to exercise control over all matters submitted for stockholder approval.

In May 2021, VisualMED entered into an acquisition agreement with Rennova to acquire certain subsidiaries owned by Rennova. This has been accounted for as a reverse acquisition in the accompanying financial statements.

On June 25, 2021, VisualMED closed the acquisition agreement with Rennova. These subsidiaries are Health Technology Solutions, Inc., Medical Mime, Inc., ClinLab, Inc., Advanced Molecular Services Group, Inc., Genomas, Inc. and CollabRx, Inc., and combined are referred to herein as HTS and AMSG (the “HTS Group”).

Products offered by the acquired entities include vCIO services, IT managed services, healthcare finance and operational business intelligence analytics dashboards, an EHR (electronic health records software), an LIS (laboratory information system), and a lab ordering and reporting software. The CollabRx and Genomas subsidiaries provided actionable data analytics and reporting for oncologists to enhance cancer diagnoses and treatment and PhyzioType Systems for DNA-guided management and prescription of drugs, respectively. These subsidiaries are not currently operating.

| 4 |

The Company operates its subsidiaries under the following structure:

In consideration for the shares of HTS and AMSG and the elimination of inter-company debt between Rennova and HTS and AMSG, the Company issued 14,000 shares of its Series B-1 Convertible Redeemable Preferred Stock (the “Series B-1 Preferred Stock”) to Rennova. The number of shares of Series B-1 Preferred Stock was subject to a post-closing adjustment which resulted in 950 additional shares of Series B-1 Preferred Stock due Rennova which were issued in September 2021. Each share of Series B-1 Preferred Stock has a stated value of $1,000 and is convertible into that number of shares of the Company’s common stock equal to the product of the stated value divided by 90% of the average closing price of the common stock during the 10 trading days immediately prior to the conversion date. Conversion of the Series B-1 Preferred Stock, however, is subject to the limitation that no conversion can be made to the extent the holder’s beneficial interest (as defined pursuant to the terms of the Series B-1 Preferred Stock) in the common stock of the Company would exceed 4.99%. The shares of Series B-1 Preferred Stock may be redeemed by the Company upon payment of the stated value of the shares plus any accrued declared and unpaid dividends. In addition, prior to the acquisition the Company’s former CEO, Gerard Dab, forgave $300,000 owed to him by the Company in exchange for the issuance of 1,000 shares of Series A-1 Preferred Stock. These shares of Series A-1 Preferred Stock were subsequently transferred to Epizon. Mr. Dab also forgave another $200,000 owed to him from the Company in exchange for 200 shares of Series C-1 Convertible Redeemable Preferred Stock (the “Series C-1 Preferred Stock”) with each share having a stated value of $1,000 and convertible into that number of shares of common stock equal to the product of the stated value divided by 90% of the average closing price of the common stock during the 10 trading days immediately prior to the conversion date. Conversion of the Series C-1 Preferred Stock is also subject to a similar 4.99% beneficial ownership limitation. Shares of the Series B-1 Preferred Stock and Series C-1 Preferred Stock were not convertible prior to the first anniversary of their issuance without the consent of the holders of a majority of the then outstanding shares, if any, of the Series A-1 Preferred Stock. Because these shares of Series B-1 Preferred Stock and Series C-1 Preferred Stock are convertible, at the option of the holder, into a variable number of common shares based solely on a fixed dollar amount (stated value) known at issuance of the shares, they have been recorded as a long-term liability at the date of issuance in accordance with ASC 480, Distinguishing Liabilities from Equity.

The following table represents the Company’s issued shares at December 31, 2022:

| Common Shares | 244,953,286 | |||

| Series A-1 Preference Shares | 1,000 | |||

| Series B-1 Preference Shares | 14,950 | |||

| Series C-1 Preference Shares | 225 |

Subsidiaries

The Company has six wholly-owned subsidiaries that provide medical support services primarily to clinical laboratories, corporate operations, rural hospitals, physician practices and behavioral health/substance abuse centers.

Health Technology Solutions, Inc. (“HTS”): HTS provides vCIO, IT managed services and data analytics dashboards to our subsidiaries and outside medical service providers. HTS operates from the corporate offices in West Palm Beach, Florida.

| 5 |

Medical Mime, Inc. (“Mime”): Mime was formed on May 9, 2014. It specializes in electronic health records (EHR) software and subscription services for the behavioral health and rehabilitation market segments. It currently serves ten behavioral health/substance abuse facilities.

ClinLab, Inc. (“ClinLab”): ClinLab develops and markets laboratory information management systems to mid-size clinical laboratories. It currently services eight clinical laboratories across the country.

AMSG owns CollabRx, Inc. (“CollabRx”) and Genomas, Inc. (“Genomas”), each of which is an inactive operation. Genomas operated a diagnostics lab until December 31, 2019, and was focused solely on the pharmacogenomics technology and platform, MedTuning, to interpret diagnostics outcomes and translate these outcomes into easily usable information to indicate the effectiveness of medications for a patient. This solution would require minimum effort to be back in operation. CollabRx owns a technology platform and database for interpreting diagnostics outcomes from cancer patients that could match the result to known treatments and or clinical trials. This solution has been dormant for a number of years and to be viable in the marketplace will require updates to the technology and the database.

Each of the subsidiaries is wholly owned by the Company and complements each other, allowing for cross selling of products and services. The Company believes the current solutions will become an added value option to a technology-based medical professional’s network communication platform to a broad range of healthcare professionals and businesses using a subscription revenue model with added value bolt on services the Company plans to develop.

In the coming year we plan to develop, acquire or license and offer a telehealth solution through partnerships in the emerging health technology sector.

Company Information

The address of our principal executive offices is 400 S. Australian Avenue, Suite 800, West Palm Beach, Florida 33401 and our telephone number at that location is (561) 421-1900.

Our website is www.innovaqor.com. The information contained on, or that may be obtained from, our website is not a part of this Annual Report on Form 10-K. We have included our website address herein solely as an inactive textual reference.

Terms of the Acquisition

Background

On June 25, 2021, the Company completed the acquisition agreement with Rennova, and acquired 100% ownership of certain subsidiaries of Rennova. The acquired businesses are now the main business of the Company.

Reasons for the Acquisition

The previous business model of the Company had not generated revenue for over five years. The Board of Directors and majority shareholders had determined the Company should pursue other opportunities for acquisition of technology and services that were similar in nature to the existing business of the Company. The Company had limited resources of cash and management and believed that an acquisition that could be completed without cash and that had its own management team would provide the best opportunity for a successful closing. The Company believes that the acquired assets and new management team create a new opportunity for the Company in a sector in which the Company’s solutions and services are in demand and should generate profitable revenue. The Company believes the acquisition brings the following benefits for shareholders:

| ● | Enhanced strategic and management focus – The acquisition will provide the Company with a well-established and accomplished management team to more effectively pursue its distinct operating priorities and strategies and enable the management to quickly and efficiently make decisions and concentrate efforts on the unique needs of each business and pursue opportunities for long-term growth and profitability. In this way, the Company’s management will be able to focus exclusively on its IT products and services business and productize its services to third parties. |

| 6 |

| ● | Direct access to capital markets – The acquisition provides the Company with a variety of existing product lines, some already generating revenue. These constitute a firm basis for supporting the Company’s business expansion. This should also mean that the Company will achieve better access to the capital markets to support a credible expansion plan. | |

| ● | Alignment of incentives with performance objectives – The acquisition will facilitate incentive compensation arrangements for employees more directly tied to the performance of the business, and may enhance employee hiring and retention by, among other things, improving the alignment of management and employee incentives with performance and growth objectives. |

The Company cannot assure you that, as a result of the acquisition, any of the benefits described above or otherwise will be realized to the extent anticipated or at all and would highlight that the acquisition adds increased risk to the Company with the following;

| ● | Increased costs – the Company will assume increased costs related to the business operations and development plan and will see an immediate increase in legal and accounting costs associated with the acquisition and the Company’s becoming fully reporting and compliant with the SEC reporting requirements. | |

| ● | The Company may experience disruptions to the business of the acquired entities as a result of the acquisition. The acquired entities had enjoyed revenue and financial assistance from related parties under its previous structure. There is no guarantee that these revenues can be retained and the acquired entities will no longer be able to rely on the support and services received prior to acquisition. | |

| ● | One-time costs of the acquisition may be significant. The Company will incur costs in connection with the acquisition that may include accounting, tax, legal and other professional services costs, recruiting, and relocation costs associated with hiring or reassigning personnel, costs related to establishing a new brand identity in the marketplace and costs to separate information systems. | |

| ● | Inability to realize anticipated benefits of the acquisition – the Company may not achieve the anticipated benefits of the acquisition for a variety of reasons, including, among others: following the acquisition, the Company may be more susceptible to market fluctuations and other adverse events. |

The prior Board of Directors concluded that the potential benefits of the acquisition outweighed the risks and concluded that it was in the best interest of the Company and its shareholders to complete the acquisition as described.

Business

InnovaQor has expertise in the areas of IT involving the design, development, creation, use and maintenance of information systems for the healthcare industry. These applications and systems will continue to improve patient care, lower costs, increase efficiency, reduce errors and improve patient outcomes. In addition, these applications and systems will accelerate and maximize reimbursements for healthcare providers.

InnovaQor also recognizes the future in interoperability (sharing data between multiple various health IT systems), telemedicine (the ability to access and interact with health data and practitioners/patients via mobile devices) and the increasing use of blockchain technologies to protect access to medical records.

We intend to develop, acquire or license and offer a medical professional’s network communication platform for medical professionals to include a talent search and telehealth solution through corporate partnerships in the emerging health technology sector.

Existing products offered by the Company’s subsidiaries are as follows:

“M2Select” is a custom built, cloud based, electronic health record which meets the needs of substance abuse treatment and behavioral health providers. M2Select’s specialized clinical workflow provides intuitive prompts for symptoms and enables you to quickly select problems and create master treatment plans with goals, objectives, and interventions. M2Select provides best-in-class patient lifecycle management for Behavioral Health/Substance Abuse (BH/SA) treatment centers. From pre-admission to billing and aftercare, M2Select is an electronic health record and patient management software that seamlessly integrates into the natural workflow of day-to-day operations.

“M2Pro” is a custom built, cloud based, electronic health record for ambulatory physician practices that meets meaningful use stage 2 and no further. Its unique dictation services further automate the workflow process for physicians allowing them to focus on their continuum of patient care. This product may also be able to be offered outside of the US market.

“ClinLab” is a turnkey client/server lab information system for mid-range laboratories. ClinLab supports interfaces to all major reference labs and the ClinLab team can provide an interface to any system with that capability. ClinLab also features an optional EHR package which enables interfacing with popular EHR systems allowing lab test results to integrate seamlessly into a provider’s EHR for an improved patient record and to fulfill the federal government requirements.

| 7 |

“Qira” is our healthcare business analytics service powered by PowerBI. It is a culmination of healthcare financial and revenue cycle management plus clinical operations oversight needs. It aggregates data from multiple healthcare systems to produce a single source business intelligence tool with executive level daily briefing to deep dive operational management of claims and operational efficiencies. There are many other analytical services available that customize solutions but none that has a proven template for success. Our competitive advantage comes from having created these tools to identify the deficiencies in the real world for the former parent Rennova from its former national laboratory operations to its more recent rural hospitals.

“vCIO Services”. Based on the skills and experience inherent within InnovaQor and resulting from work undertaken on behalf of the former parent, Rennova, InnovaQor offers a range of CIO services centered on our ability to link IT systems to business objectives combined with our knowledge of technology trends likely to impact our sector. The CIO services would include (but not be limited to):

| ● | Program and Project Management | |

| ● | Vendor Management | |

| ● | Business Continuity and Disaster Recovery | |

| ● | Security Services | |

| ● | Network Infrastructure Management | |

| ● | Helpdesk Provision |

“MedTuning” is the technology and platform owned by Genomas. It utilized proprietary biomarkers, treatment algorithms, and a web-based interactive physician portal delivery system to provide clinical decision support for physicians and personalized drug treatment for patients. Products were DNA-guided to improve the therapeutic benefit of widely used prescription drugs while also reducing the risk of significant side effects for patients.

Medical Informatics: Our technology platform, proprietary algorithms and physician interface portal can be extended to a wide range of drug categories.

Research and Development: Technology platform applicable to numerous disease states; current pipeline in mental health, pain management, cardiovascular and diabetes.

“Advantage” is a proprietary HIPAA compliant software developed to eliminate the need for paper requisitions by providing an easy to use and efficient web-based system that lets customers securely place lab orders, track samples and view test reports in real time from any web-enabled laptop, notepad or smart phone.

Brands

We intend to trademark both InnovaQor and its products and services, i.e. ClinLab, M2Select, Qira, vCIO and Health Technology Solutions.

Sales

The Company has the following wholly owned subsidiaries, which it purchased on June 25, 2021: Health Technology Solutions, Inc., Medical Mime, Inc., ClinLab, Inc., Advanced Molecular Services Group, Inc. (“AMSG”), Genomas, Inc. and CollabRx, Inc. These subsidiaries provided products and services to 25 and 36 customers in the United States and generated $343,440 and $468,883 (including $191,517 and $237,551 from a related party) in net revenues during the years ended December 31, 2022 and 2021, respectively.

InnovaQor intends to sell its Health Technology Solutions, Medical Mime and ClinLab products and services directly to customers through internal sales and digital marketing. InnovaQor intends to identify strategic partnerships that sell into the sectors it is targeting. InnovaQor intends to promote these products and services to the strategic partnerships’ existing clientele coming to agreement on a recurring revenue based on cash collected for closed sales of these products and services.

Competitive Position

The healthcare software, IT and vCIO consulting services industry is extremely competitive, highly fragmented, and subject to rapid change. The industry includes a large number of participants with a variety of skills and industry expertise, including other strategy, business operations, technology, technical advisory firms, regional and specialty consulting firms, and the internal professional resources of organizations. We compete with a large number of service and technology providers in all of our segments. Our competitors often vary, depending on the particular practice area. We expect to continue to face competition from new entrants.

| 8 |

We believe the principal competitive factors in our market include reputation, the ability to attract and retain top talent, and the capacity to manage engagements effectively to drive high value to clients. There is also competition on price, although to a lesser extent due to the criticality of the issues that many of our services address. Our competitors often have a greater geographic footprint, a broader international presence, and more resources than we do, but we believe that our industry experience and reputation, ability to deliver meaningful client results, and balanced portfolio of services enable us to compete favorably in the consulting marketplace.

Our rehab EHR product, Medical Mime, is a main competitor in its sector and our immediate competition is provided by KIPU, BestNotes, Zencharts, Sunwave, and TherapyNotes. Our competitive advantage is a system developed with and for facilities practicing in this sector along with customized reports and forms. Our system offers partially automated implementation and fully automated billing files that restrict billing until all required documentation is available while flagging operational deficiencies.

Our LIS, ClinLab, is a small player in its sector and our immediate competitors are LabDaq, Schuyler House and RelayMed. Our competitive advantage is a select feature set and affordability.

Our vCIO services are just launching and have the experience of being the internal IT team for the former parent company, Rennova. With a 10-year experience in providing complete services, consulting, project management, software management, vendor management and network engineering, vCIO will specialize in healthcare facilities.

Qira is our healthcare business analytics tool powered by PowerBI. It is a culmination of healthcare financial and revenue cycle management plus clinical operations operational oversight needs. It aggregates data from multiple healthcare systems to produce a single source business intelligence tool with executive level daily briefing to deep dive operational management of claims and operational efficiencies. There are many other analytical services available that customize solutions but none that has a proven template for success. Our competitive advantage comes from having created these tools to identify the deficiencies in the real world for the former parent Rennova from its former national laboratory operations to its more recent rural hospitals. This product easily pays for itself as it immediately eliminates the need for accountants’ monthly delivery of numbers that can cost upwards of $25,000 a month.

Research and Development

The industries and market segments in which we plan to operate and compete are subject to rapid technological developments, evolving industry standards, changes in customer requirements and competitive new products and features. As a result, we believe our success, in part, will depend on our ability to build and enhance our products in a timely and efficient manner and to develop and introduce new products that meet our clients’ needs and help our clients reduce their total cost of operation. To achieve these objectives, we plan to make research and development investments through internal and third-party development activities, third-party licensing agreements and potentially through joint ventures and acquisitions.

Research and Intellectual Property

Our future success and ability to compete will depend on our ability to develop and maintain our intellectual property and proprietary technology and to operate without infringing on the proprietary rights of others. Software products are generally licensed to customers on a non-exclusive basis for internal use in a customer’s organization. We plan to also grant rights in intellectual property that we plan on developing or acquiring to third parties to allow them to market certain of our future products on a non-exclusive or limited-scope exclusive basis for an application of such product or to a specific geographic region.

InnovaQor plans to protect its intellectual property in its subsidiaries through a combination of trademarks and copyrights in the coming year. InnovaQor will evaluate the possibility of acquiring or developing patents that are related to healthcare services and products.

Our IP strategy encompasses protection on composition of matter and method for DNA markers, marker ensembles, and predictive biostatistical algorithms.

| 9 |

Platform Technology

Trademarks and Copyrights

U.S. Copyright (Registration Number VA 1-797-692): Personalized Health Portal with design, user interface and algorithm.

While we believe our intellectual property will be an asset, and our ability to maintain and protect our intellectual property rights is important to our success, we do not anticipate that our business will be materially dependent on any patent, trademark, license, or other intellectual property right.

Employees

As of March 30, 2023, we have six employees, five of whom are working on maintenance and customer service of our existing products. We expect to grow with a focus on sales and business development eventually expanding our technical team to support the growth. We plan to hire a team of employees and contractors to deliver on the goal of developing and delivering a technology-based communication platform to a broad range of healthcare professionals and businesses using a subscription revenue model with added value bolt on services.

Cyclical Nature of the Business

We have found that our business is not very cyclical but it does exhibit certain seasonality around holiday periods.

Regulatory Matters

The healthcare industry is subject to extensive government regulation, most notably the Health Insurance Portability and Accountability Act (HIPAA) and Protected Health Information (PHI). HIPAA helps protect the privacy of patient information by:

| ● | Providing the ability to transfer and continue health insurance coverage for millions of American workers and their families when they change or lose their jobs; | |

| ● | Reducing health care fraud and abuse; | |

| ● | Mandating industry-wide standards for health care information on electronic billing and other processes; and | |

| ● | Requiring the protection and confidential handling of protected health information |

PHI is a HIPAA Privacy Rule that provides federal protections for personal health information held by covered entities and gives patients an array of rights with respect to that information. At the same time, the Privacy Rule is balanced so that it permits the disclosure of personal health information needed for patient care and other important purposes.

Although the standards are challenging, we believe that our products are compliant with HIPAA and PHI regulations. Nonetheless, our Company could be adversely affected if a third party is impacted by HIPAA or PHI related software defects.

Emerging Growth Company Status of InnovaQor

An emerging growth company (EGC) is any company that meets the following requirements and will lose its emerging growth status should it exceed any of these:

| ● | The company has less than $1.07 billion or more of total gross revenue in a consecutive 12-month period; | |

| ● | Is within five years of its original IPO; | |

| ● | The company cannot have issued more than $1 billion in non-convertible bonds within the last three years; and | |

| ● | The company does not qualify as a large accelerated filer, meaning having a public float of over $700 million. |

InnovaQor is an “emerging growth company” as defined in the Jumpstart our Business Startups Act (the “JOBS Act”). As such, InnovaQor will be eligible to take advantage of certain exemptions from various reporting requirements that apply to other public companies that are not emerging growth companies, including compliance with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act and the requirements to hold a non-binding advisory vote on executive compensation and any golden parachute payments not previously approved. If InnovaQor does take advantage of some or all of these exemptions, some investors may find its common stock less attractive. The result may be a less active trading market for the common stock and its stock price may be more volatile.

| 10 |

In addition, Section 107 of the JOBS Act provides that an emerging growth company may take advantage of the extended transition period provided in Section 13(a) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), for complying with new or revised accounting standards, meaning that InnovaQor, as an emerging growth company, can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. It is InnovaQor’s present intention to adopt any applicable accounting standards timely. If at some time InnovaQor delays adoption of a new or revised accounting standard, our financial statements may not be comparable to those of companies that comply with such new or revised accounting standards.

Item 1A: Risk Factors An investment in our common stock is highly speculative and involves a high degree of risk. In determining whether to purchase InnovaQor’s common stock, an investor should carefully consider all of the material risks described below, together with the other information contained in this report. An investor should only purchase InnovaQor’s securities if he or she can afford to suffer the loss of his or her entire investment.

General Business and Industry Risks

An inability to retain our senior management team would be detrimental to the success of our business.

We rely heavily on our senior management team; our ability to retain them is particularly important to our future success. Given the highly specialized nature of our services (Healthcare, IT), the senior management team must have a thorough understanding of our product and service offerings as well as the skills and experience necessary to manage an organization consisting of a diverse group of professionals and external parties. In addition, we rely on our senior management team to generate and market our business successfully in a crowded, complex and legislatively bound marketplace. Further, our senior management’s personal reputations and relationships with our clients are a critical element in obtaining and maintaining client engagements. We will enter into non-solicitation agreements with our senior management team, and we will also enter into well-scoped non-competition agreements. If one or more members of our senior management team leave and we cannot replace them with a suitable candidate quickly, we could experience difficulty in securing and successfully completing engagements and managing our business properly, which could harm our business prospects and results of operations.

Our inability to hire and retain talented people in an industry where there is great competition for talent could have a serious negative effect on our prospects and results of operations.

Our business involves the delivery of software products and professional services and is labor intensive. Our success depends largely on our general ability to attract, develop, motivate, and retain highly skilled professionals. Further, we must successfully maintain the right mix of professionals with relevant experience and skill sets as we grow, as we expand into new service offerings, and as the market evolves. The loss of a significant number of our professionals, the inability to attract, hire, develop, train, and retain additional skilled personnel, or the failure to maintain the right mix of professionals could have a serious negative effect on us, including our ability to manage, staff, and successfully complete our existing engagements and obtain new engagements. Qualified professionals are in great demand, and we face significant competition for both senior and junior professionals with the requisite credentials and experience. Our principal competition for talent comes from other software and consulting firms as well as from organizations seeking to staff their internal professional positions. Many of these competitors may be able to offer significantly greater compensation and benefits or more attractive lifestyle choices, career paths, or geographic locations than we do. Therefore, we may not be successful in attracting and retaining the skilled persons we require to conduct and expand our operations successfully. Increasing competition for these revenue-generating professionals may also significantly increase our labor costs, which could negatively affect our margins and results of operations.

Additional hiring, departures, business acquisitions and dispositions could disrupt our operations, increase our costs or otherwise harm our business.

Our business strategy is dependent in part upon our ability to grow by hiring individuals or groups of individuals and by acquiring complementary businesses. However, we may be unable to identify, hire, acquire, or successfully integrate new employees and acquired businesses without substantial expense, delay, or other operational or financial obstacles. From time to time, we will evaluate the total mix of products and services we provide and we may conclude that businesses may not achieve the results we previously expected. Competition for future hiring and acquisition opportunities in our markets could increase the compensation we offer to potential employees or the prices we pay for businesses we wish to acquire. In addition, we may be unable to achieve the financial, operational, and other benefits we anticipate from any hiring or acquisition, as well as any disposition, including those we have completed so far. New acquisitions could also negatively impact existing practices and cause current employees to depart. Hiring additional employees or acquiring businesses could also involve a number of additional risks, including:

| ● | the diversion of management’s time, attention, and resources from managing and marketing our Company; |

| 11 |

| ● | the failure to retain key acquired personnel or existing personnel who may view the acquisition unfavorably; | |

| ● | the potential loss of clients of acquired businesses; | |

| ● | the need to compensate new employees while they wait for their restrictive covenants with other institutions to expire; | |

| ● | the potential need to raise significant amounts of capital to finance a transaction or the potential issuance of equity securities that could be dilutive to our existing shareholders; | |

| ● | increased costs to improve, coordinate, or integrate managerial, operational, financial, and administrative systems; | |

| ● | the potential assumption of liabilities of an acquired business; | |

| ● | the inability to attain the expected synergies with an acquired business; | |

| ● | the usage of earn-outs based on the future performance of our business acquisitions may deter the acquired company from fully integrating into our existing business; | |

| ● | the perception of inequalities if different groups of employees are eligible for different benefits and incentives or are subject to different policies and programs; and | |

| ● | difficulties in integrating diverse backgrounds and experiences of consultants, including if we experience a transition period for newly hired consultants that results in a temporary drop in our utilization rates or margins. |

Determining the fair value of a reporting unit requires us to make significant judgments, estimates, and assumptions. While we believe that the estimates and assumptions underlying our valuation methodology are reasonable, these estimates and assumptions could have a significant impact on whether or not a non-cash goodwill impairment charge is recognized and also the magnitude of any such charge. The results of an impairment analysis are as of a point in time. There is no assurance that the actual future earnings or cash flows of our reporting units will be consistent with our projections. We will monitor any changes to our assumptions and will evaluate goodwill as deemed warranted during future periods. Any significant decline in our operations could result in non-cash goodwill impairment charges.

Changes in capital markets, legal or regulatory requirements, and general economic or other factors beyond our control could reduce demand for our services, in which case our revenues could decline.

A number of factors outside of our control affect demand for our services. These include:

| ● | fluctuations in the U.S. economy; | |

| ● | the U.S. or global financial markets and the availability, costs, and terms of credit; | |

| ● | changes in laws and regulations; and | |

| ● | other economic factors and general business conditions. |

We are not able to predict the positive or negative effects that future events or changes to the U.S. economy, financial markets, or regulatory and business environment could have on our operations.

Changes in U.S. tax laws could have a material adverse effect on our business, cash flow, results of operations and financial conditions.

We are subject to income and other taxes in the U.S. at the state and federal level. Changes in applicable U.S. state or federal tax laws and regulations, or their interpretation and application, could materially affect our tax expense and profitability. The Company has not filed its federal tax returns for more than 10 years. The Company does not anticipate material adjustments of its tax liabilities when such returns are filed, but there is no guarantee that such filings will not have a material adverse effect.

| 12 |

Acquisition of the HTS Group has presented and will continue to present management with new challenges that did not exist under the umbrella of its former parent.

Under the former parent, management had the support of an experienced financial team, HR support and support for SEC filings. This support system does not currently exist in the current company and new challenges are presenting themselves every day. The immature knowledge and experience in these areas are likely to take longer to complete actions and will take management’s attention away from the day to day operations where it is needed to improve revenues.

If we are unable to manage fluctuations in our business successfully, we may not be able to achieve profitability.

To successfully manage growth, we must periodically adjust and strengthen our operating, financial, accounting, and other systems, procedures, and controls, which could increase our costs and may adversely affect our gross profits and our ability to achieve profitability if we do not generate increased revenues to offset the costs. As a public company, our information and control systems must enable us to prepare accurate and timely financial information and other required disclosures. If we discover deficiencies in our existing information and control systems that impede our ability to satisfy our reporting requirements, we must successfully implement improvements to those systems in an efficient and timely manner.

The nature of our services and the general economic environment make it difficult to predict our future operating results. To achieve profitability, we must:

| ● | attract, integrate, retain, and motivate highly qualified professionals; | |

| ● | achieve and maintain adequate utilization and suitable billing rates for our revenue-generating professionals; | |

| ● | expand our existing relationships with our clients and identify new clients in need of our services; | |

| ● | successfully resell products/engagements and secure new client sales/engagements every year; | |

| ● | maintain and enhance our brand recognition; and | |

| ● | adapt quickly to meet changes in our markets, our business mix, the economic environment, the credit markets, and competitive developments. |

Our financial results could suffer if we are unable to achieve or maintain adequate utilization and suitable billing rates for our products and services.

Our profitability depends to a large extent on the utilization and billing rates of our professionals. Utilization of our professionals is affected by a number of factors, including:

| ● | the number and size of client sales/engagements; | |

| ● | the timing of the commencement, completion and termination of engagements, which in many cases is unpredictable; | |

| ● | our ability to transition our consultants efficiently from completed engagements to new engagements; | |

| ● | the hiring of additional consultants because there is generally a transition period for new consultants that results in a temporary drop in our utilization rate; | |

| ● | unanticipated changes in the scope of client engagements; | |

| ● | our ability to forecast demand for our services and thereby maintain an appropriate level of consultants; and | |

| ● | conditions affecting the industries in which we practice as well as general economic conditions. |

The billing rates of our consultants that we are able to charge are also affected by a number of factors, including:

| ● | our clients’ perception of our ability to add value through our products/services; | |

| ● | the market demand for the products/services we provide; | |

| ● | an increase in the number of sales/engagements in the government sector, which are subject to federal contracting regulations; | |

| ● | introduction of new products/services by us or our competitors; | |

| ● | our competition and the pricing policies of our competitors; and | |

| ● | current economic conditions. |

If we are unable to achieve and maintain adequate overall utilization as well as maintain or increase the billing rates for our consultants, our financial results could materially suffer. In addition, our consultants may need to perform services at the physical locations of our clients. If there are natural disasters, disruptions to travel and transportation or problems with communications systems, our ability to perform services for, and interact with, our clients at their physical locations may be negatively impacted which could have an adverse effect on our business and results of operations.

| 13 |

It is likely that our quarterly results of operations may fluctuate in the future as a result of certain factors, some of which may be outside of our control.

A key element of our strategy is to market our products and services directly to certain specific organizations, such as health systems and hospitals, and to increase the number of our products and services utilized by existing clients. The sales cycle for some of our products and services is often lengthy and may involve significant commitment of client personnel. As a consequence, the commencement date of a client engagement often cannot be accurately forecasted. Certain of our client contracts contain terms that result in revenue that is deferred and cannot be recognized until the occurrence of certain events. As a result, the period of time between contract signing and recognition of associated revenue may be lengthy, and we are not able to predict with certainty the period in which revenue will be recognized.

Certain of our contracts provide that some portion or all of our fees are at risk if our services do not result in the achievement of certain performance targets. To the extent that any revenue is contingent upon the achievement of a performance target, we only recognize revenue upon client confirmation that the performance targets have been achieved. If a client fails to provide such confirmation in a timely manner, our ability to recognize revenue will be delayed.

Fee discounts, pressure to not increase or even decrease our rates, and less advantageous contract terms could result in the loss of clients, lower revenues and operating income, higher costs, and less profitable engagements. More discounts or write-offs than we expect in any period would have a negative impact on our results of operations.

Other fluctuations in our quarterly results of operations may be due to a number of other factors, some of which are not within our control, including:

| ● | the timing and volume of client invoices processed and payments received, which may affect the fees payable to us under certain of our engagements; | |

| ● | client decisions regarding renewal or termination of their contracts; | |

| ● | the amount and timing of costs related to the development or acquisition of technologies or businesses; and | |

| ● | unforeseen legal expenses, including litigation and other settlement gains or losses. |

The profitability of our fixed-fee engagements with clients may not meet our expectations if we underestimate the cost of these engagements.

When making proposals for fixed-fee engagements, we estimate the costs and timing for completing the engagements. These estimates reflect our best judgment regarding the efficiencies of our methodologies and consultants as we plan to deploy them on engagements. Any increased or unexpected costs or unanticipated delays in connection with the performance of fixed-fee engagements, including delays caused by factors outside our control, could make these contracts less profitable or unprofitable, which would have an adverse effect on our profit margin.

Our business is becoming increasingly dependent on information technology and will require additional investments in order to grow and meet the demands of our clients.

We depend on the use of sophisticated technologies and systems. Some of services may become dependent on the use of software applications and systems that we do not own and could become unavailable. Moreover, our technology platforms will require continuing investments by us in order to expand existing service offerings and develop complementary services. Our future success depends on our ability to adapt our services and infrastructure while continuing to improve the performance, features, and reliability of our services in response to the evolving demands of the marketplace.

| 14 |

Adverse changes to our relationships with key third-party vendors, or in the business of our key third-party vendors, could unfavorably impact our business.

A portion of our services and solutions depends on technology or software provided by third-party vendors. Some of these third-party vendors refer potential clients to us, and others require that we obtain their permission prior to accessing their software. These third- party vendors could terminate their relationship with us without cause and with little or no notice, which could limit our service offerings and harm our financial condition and operating results. In addition, if a third-party vendor’s business changes or is reduced, that could adversely affect our business. Moreover, if third-party technology or software that is important to our business does not continue to be available or utilized within the marketplace, or if the services that we provide to clients are no longer relevant in the marketplace, our business may be unfavorably impacted.

We could experience system failures, service interruptions, or security breaches that could negatively impact our business.

Our organization is comprised of employees who work on matters throughout the United States. We may be subject to disruption to our operating systems from technology events that are beyond our control, including the possibility of failures at third-party data centers, disruptions to the Internet, natural disasters, power losses, and malicious attacks. In addition, despite the implementation of security measures, our infrastructure and operating systems, including the Internet and related systems, may be vulnerable to physical break-ins, hackers, improper employee or contractor access, computer viruses, programming errors, denial-of-service attacks, or other attacks by third parties seeking to disrupt operations or misappropriate information or similar physical or electronic breaches of security. While we have taken and are taking reasonable steps to prevent and mitigate the damage of such events, including implementation of system security measures, information backup, and disaster recovery processes, those steps may not be effective and there can be no assurance that any such steps can be effective against all possible risks. We will need to continue to invest in technology in order to achieve redundancies necessary to prevent service interruptions. Access to our systems as a result of a security breach, the failure of our systems, or the loss of data could result in legal claims or proceedings, liability, or regulatory penalties and disrupt operations, which could adversely affect our business and financial results.

Our reputation could be damaged and we could incur additional liabilities if we fail to protect client and employee data through our own accord or if our information systems are breached.

We rely on information technology systems to process, transmit, and store electronic information and to communicate among our locations and with our clients, partners, and employees. The breadth and complexity of this infrastructure increases the potential risk of security breaches which could lead to potential unauthorized disclosure of confidential information.

In providing services to clients, we may manage, utilize, and store sensitive or confidential client or employee data, including personal data and protected health information. As a result, we are subject to numerous laws and regulations designed to protect this information, such as the U.S. federal and state laws governing the protection of health or other personally identifiable information, including the Health Insurance Portability and Accountability Act (HIPAA). In addition, many states, and U.S. federal governmental authorities have adopted, proposed or are considering adopting or proposing, additional data security and/or data privacy statutes or regulations. Continued governmental focus on data security and privacy may lead to additional legislative and regulatory action, which could increase the complexity of doing business. The increased emphasis on information security and the requirements to comply with applicable U.S. data security and privacy laws and regulations may increase our costs of doing business and negatively impact our results of operations.

These laws and regulations are increasing in complexity and number. If any person, including any of our employees, negligently disregards or intentionally breaches our established controls with respect to client or employee data, or otherwise mismanages or misappropriates that data, we could be subject to significant monetary damages, regulatory enforcement actions, fines, and/or criminal prosecution.

In addition, unauthorized disclosure of sensitive or confidential client or employee data, whether through systems failure, employee negligence, fraud, or misappropriation, could damage our reputation and cause us to lose clients and their related revenue in the future.

| 15 |

Changes in capital markets, legal or regulatory requirements, general economic conditions and monetary or geo-political disruptions, as well as other factors beyond our control, could reduce demand for our practice offerings or services, in which case our revenues and profitability could decline.

Different factors outside of our control could affect demand for our practices and our services. These include:

| ● | fluctuations in the U.S. economy, including economic recessions and the strength and rate of any general economic recoveries; | |

| ● | the U.S. financial markets and the availability, costs and terms of credit and credit modifications; | |

| ● | business and management crises, including the occurrence of alleged fraudulent or illegal activities and practices; | |

| ● | new and complex laws and regulations, repeals of existing laws and regulations or changes of enforcement of laws, rules and regulations; | |

| ● | other economic, geographic or political factors; and | |

| ● | general business conditions. |

We are not able to predict the positive or negative effects that future events or changes to the U.S. economy will have on our business. Fluctuations, changes and disruptions in financial, credit, mergers and acquisitions and other markets, political instability and general business factors could impact various operations and could affect such operations differently. Changes to factors described above, as well as other events, including by way of example, contractions of regional economies, monetary systems, banking, real estate and retail or other industries; debt or credit difficulties or defaults by businesses; new, repeals of or changes to laws and regulations, including changes to the bankruptcy and competition laws of the U.S.; tort reform; banking reform; a decline in the implementation or adoption of new laws of regulation, or in government enforcement, litigation or monetary damages or remedies that are sought; or political instability may have adverse effects on our business.

Our revenues, operating income and cash flows are likely to fluctuate.

We expect to experience fluctuations in our revenues and cost structure and the resulting operating income and cash flows. We may experience fluctuations in our annual and quarterly financial results, including revenues, operating income and earnings per share, for reasons that include (i) the types and complexity, number, size, timing and duration of client engagements; (ii) the timing of revenue recognition under accounting principles generally accepted in the United States of America (“U.S. GAAP”); (iii) the utilization of revenue-generating professionals, including the ability to adjust staffing levels up or down to accommodate our business and prospects; (iv) the time it takes before a new hire becomes profitable; (v) the geographic locations of our clients or the locations where services are rendered; (vi) billing rates and fee arrangements, including the opportunity and ability to successfully reach milestones and complete projects, and collect for them; (vii) the length of billing and collection cycles and changes in amounts that may become uncollectible; (viii) changes in the frequency and complexity of government regulatory and enforcement activities; and (ix) economic factors beyond our control.

We may also experience fluctuations in our operating income and related cash flows because of increases in employee compensation, including changes to our incentive compensation structure and the timing of incentive payments. Also, the timing of investments or acquisitions and the cost of integrating them may cause fluctuations in our financial results, including operating income and cash flows. This volatility may make it difficult to forecast our future results with precision and to assess accurately whether increases or decreases in any one or more quarters are likely to cause annual results to exceed or fall short of expectations.

If we do not effectively manage the utilization of our professionals or billable rates, our financial results could decline.

Our failure to manage the utilization of our professionals who bill on an hourly basis, or maintain or increase the hourly rates we charge our clients for our services, could result in adverse consequences, such as non- or lower-revenue-generating professionals, increased employee turnover, fixed compensation expenses in periods of declining revenues, the inability to appropriately staff engagements (including adding or reducing staff during periods of increased or decreased demand for our services), or special charges associated with reductions in staff or operations. Reductions in workforce or increases of billable rates will not necessarily lead to savings. In such events, our financial results may decline or be adversely impacted. A number of factors affect the utilization of our professionals. Some of these factors we cannot predict with certainty, including general economic and financial market conditions; the complexity, number, type, size and timing of client engagements; the level of demand for our services; appropriate professional staffing levels, in light of changing client demands and market conditions; and competition and acquisitions. In addition, any expansion into or within locations where we are not well known or where demand for our services is not well-developed could also contribute to low or lower utilization rates.

InnovaQor may enter into engagements which involve non-time and material arrangements, such as fixed fees and time and materials with caps. Failure to effectively manage professional hours and other aspects of alternative fee engagements may result in the costs of providing such services exceeding the fees collected by InnovaQor. Failure to successfully complete or reach milestones with respect to contingent fee or success fee assignments may also lead to lower revenues or the costs of providing services under those types of arrangements may exceed the fees collected by InnovaQor.

| 16 |

We may receive requests to discount our fees or to negotiate lower rates for our services and to agree to contract terms relative to the scope of services and other terms that may limit the size of an engagement or our ability to pass through costs. We will consider these requests on a case-by-case basis. In addition, our clients and prospective clients may not accept rate increases that we put into effect or plan to implement in the future. Fee discounts, pressure not to increase or even decrease our rates, and less advantageous contract terms could result in the loss of clients, lower revenues and operating income, higher costs and less profitable engagements. More discounts or write-offs than we expect in any period would have a negative impact on our results of operations. There is no assurance that significant client engagements will be renewed or replaced in a timely manner or at all, or that they will generate the same volume of work or revenues, or be as profitable as past engagements.

Our Company faces certain risks, including (i) industry consolidation and a heightened competitive environment, (ii) downward pricing pressure, (iii) technology changes and obsolescence, (iv) failure to protect client information against cyber-attacks and (v) failure to protect IP, which individually or together could cause the financial results and prospects of the Company to decline.

Our Company is facing significant competition from other consulting and/or software providers. There continues to be significant consolidation of companies providing products and services similar to those offered by our Company, which may provide competitors access to greater financial and other resources than those of InnovaQor. This industry is subject to significant and rapid innovation. Larger competitors may be able to invest more in research and development, react more quickly to new regulatory or legal requirements and other changes, or innovate more quickly and efficiently. Our Medical Mime and ClinLab software have been facing significant competition from competing software products.

The software and products of our Company are subject to rapid technological innovation. There is no assurance that we will successfully develop new versions of our Medical Mime and ClinLab software or other products. Our software may not keep pace with necessary changes and innovation. There is no assurance that new, innovative or improved software or products will be developed, compete effectively with the software and technology developed and offered by competitors, be price competitive with other companies providing similar software or products, or be accepted by our clients or the marketplace. If InnovaQor is unable to develop and offer competitive software and products or is otherwise unable to capitalize on market opportunities, the impact could adversely affect our operating margins and financial results.

Our reputation for providing secure information storage and maintaining the confidentiality of proprietary, confidential and trade secret information is critical to the success of our Company, which hosts client information as a service. We may face cyber-based attacks and attempts by hackers and similar unauthorized users to gain access to or corrupt our information technology systems. Such attacks could disrupt our business operations, cause us to incur unanticipated losses or expenses, and result in unauthorized disclosures of confidential or proprietary information. Although we seek to prevent, detect and investigate these network security incidents, and have taken steps to mitigate the likelihood of network security breaches, there can be no assurance that attacks by unauthorized users will not be attempted in the future or that our security measures will be effective.

We rely on a combination of copyrights, trademarks, trade secrets, confidentiality and other contractual provisions to protect our assets. Our software and related documentation will be protected principally under trade secret and copyright laws, which afford only limited protection, and the laws of some foreign jurisdictions provide less protection for our proprietary rights than the laws of the U.S. Unauthorized use and misuse of our IP by employees or third parties could have a material adverse effect on our business, financial condition and results of operations. The available legal remedies for unauthorized or misuse of our IP may not adequately compensate us for the damages caused by unauthorized use.

If we (i) fail to compete effectively, including by offering our software and services at a competitive price, (ii) are unable to keep pace with industry innovation and user requirements, (iii) are unable to replace clients or revenues as engagements end or are canceled or the scope of engagements are curtailed, or (iv) are unable to protect our clients’ or our own IP and proprietary information, the financial results of InnovaQor would be adversely affected. There is no assurance that we can replace clients or the revenues from engagements, eliminate the costs associated with those engagements, find other engagements to utilize our professionals, develop competitive products or services that will be accepted or preferred by users, offer our products and services at competitive prices, or continue to maintain the confidentiality of our IP and the information of our clients.

| 17 |

We may not manage our growth effectively, and our profitability may suffer.

Periods of expansion may strain our management team, or human resources and information systems. To manage growth successfully, we may need to add qualified managers and employees and periodically update our operating, financial and other systems, as well as our internal procedures and controls. We also must effectively motivate, train and manage a larger professional staff. If we fail to add or retain qualified managers, employees and contractors when needed, estimate costs, or manage our growth effectively, our business, financial results and financial condition may suffer.

We cannot assure that we can successfully manage growth through acquisitions and the integration of the companies and assets we acquire or that they will result in the financial, operational and other benefits that we anticipate. Some acquisitions may not be immediately accretive to earnings, and some expansion may result in significant expenditures.

In periods of declining growth, underutilized employees and contractors may result in expenses and costs being a greater percentage of revenues. In such situations, we will have to weigh the benefits of decreasing our workforce or limiting our service offerings and saving costs against the detriment that InnovaQor could experience from losing valued professionals and their industry expertise and clients.

We may not secure the capital required to develop our business.

Our business is dependent on securing additional capital. If we fail to secure the required capital our business will fail.

Reliance on related party

We rely heavily on Rennova, the former owner of our subsidiaries, for our current revenues and for the provision of loans necessary for us to operate our business until we secure our own capital. A loss of the contracts for service with Rennova or a loss of financial support would have a material adverse effect on our operations and business.

Going Concern Risk Factor

Although our financial statements have been prepared on a going concern basis, we have accumulated significant losses and have negative cash flows from operations that could adversely affect our ability to secure additional capital to fund our operations or limit our ability to react to changes in the economy or our industry. These or additional risks or uncertainties not presently known to us, or that we currently deem immaterial, raise substantial doubt about our ability to continue as a going concern.

Under Accounting Standards Update (“ASU”) 2014-15, Presentation of Financial Statements—Going Concern (Subtopic 205-40) Accounting Standards Codification (“ASC 205-40”), InnovaQor has the responsibility to evaluate whether conditions and/or events raise substantial doubt about its ability to meet its future financial obligations as they become due within one year after the date that the financial statements are issued. As required by ASC 205-40, this evaluation shall initially not take into consideration the potential mitigating effects of plans that have not been fully implemented as of the date the financial statements are issued. Management has assessed InnovaQor’s ability to continue as a going concern in accordance with the requirement of ASC 205-40.